What is hypotax and what is its purpose?

You don’t need to be a tax expert to know that different countries tax individuals’ incomes at widely differing rates. Many western European countries are well known for applying marginal rates approaching 50% or more, whereas Gulf states like Qatar levy no income tax at all.

When an employee moves abroad, they will most likely become subject to a new tax regime in the host country and the base on which tax is calculated is often increased by assignment-related payments and benefits. Home country tax liabilities may also continue. The approach companies take to taxation can therefore have a significant effect on the employee’s overall remuneration package. Companies who ignore the difference in tax levels between two countries may find positions in high-tax locations hard to fill while low tax jurisdictions are oversubscribed.

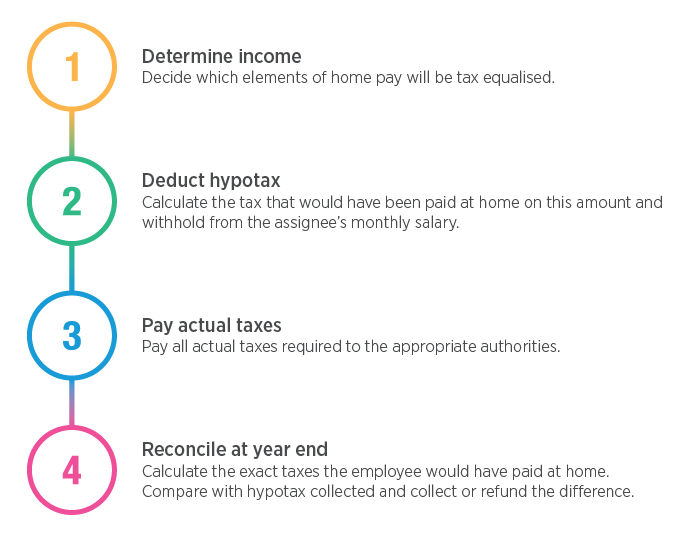

To promote mobility and ensure equity between assignees globally, 72% of companies using a home-based approach to assignment pay employ a tax equalisation policy, according to ECA’s latest Expatriate Salary Management Survey. The home-based approach is intended to keep the link with the assignee’s home country to ensure they are no worse off when on assignment. Tax equalisation allows for employees on assignment to effectively pay the same amount of tax they would have paid had they remained at home. This ‘stay at home’ tax figure is known as hypothetical tax (or hypotax).

What income is hypothetically taxed?

As hypotax is, by definition, hypothetical, its method of calculation is not enshrined in tax law and must instead be determined by company policy. A balance is needed between accurately estimating home country taxes while standardising procedures to facilitate administration and promote employee equity. Containing costs will also play a role. As each organisation’s expatriate demography, corporate strategy and budget are different from the next, each will strike a different balance.

Generally, the starting point is the notional home gross salary. Added to this are any additional allowances and benefits-in-kind normally received in the home country. A few companies go further and include personal income or even spousal income.

Guaranteed bonuses should be included; some companies will also include non-guaranteed bonuses to ensure that sufficient tax is withheld in the event of such a payment, rather than having to reclaim it from the assignee upon reconciliation.

As the principle of hypotax is to maintain home country tax levels, benefits specifically relating to the move (e.g. cost of living allowances, host country housing etc.) should not be included.

How is hypotax calculated?

The gross income figure is then netted down for home country tax and, in most cases, social security contributions. This is the hypotax that the employee will pay on assignment. One way to net down is to use an individual’s actual tax figure, perhaps taken from the home country payroll or precisely calculated according to their individual circumstances.

This case-by-case approach may work well for a company with a few assignees, but could prove time-consuming and costly where there is a large expatriate workforce and is difficult to do if the employee is no longer taxable in the home country. It also raises equity issues. Personal factors (deductions for mortgage interest, alimony etc.) are not considered when determining home country salaries, so how can their inclusion in the host country salary be justified?

Using a standardised methodology avoids employees on equal home salaries receiving widely different assignment salaries. It can also help curtail discussions with assignees about what should and shouldn’t be included in the calculations. Most companies therefore net down using a set of standard assumptions for all their assignees, although actual family size is usually taken into account. Some countries provide financial relief for families as cash allowances through social security rather than the tax system, so family allowance benefits can be included in hypotax calculations where entitlement ceases on assignment.

In addition to the standard assumptions applicable to all individuals, companies may wish to incorporate certain non-standard reliefs or benefits into hypotax if most of their expatriate workforce receives them.

Pension contributions often attract tax relief and some companies providing occupational plans include this relief in hypotax. However, they could be penalising individuals with private pension arrangements, as their tax relief is ignored unless the employer takes these personal factors into account.

What happens next?

Under tax equalisation the employer takes responsibility for paying the actual taxes due from the employee in both the home and host jurisdictions and withholds the estimated hypothetical tax from the assignee’s salary each month. At the end of the tax year, it is common to carry out a reconciliation comparing the precise amount of tax the employee would have paid had they stayed at home with the hypotax collected. The difference is then recovered from or refunded to the employee as appropriate.

FIND OUT MORE

Clear and comprehensive tax reports are available for more than 100 countries as part of a subscription to ECA data and can also be bought on demand.

ECA’s hypothetical tax data is built into our various assignment calculators and cost projections, including our assignment management system, ECAEnterprise. Our Tax Calculator enables you to calculate hypotax at the touch of a button, or alternatively we can run tax calculations on your behalf.

Download our tax and social security white paper to find out more about how personal income tax levels vary around the world.

Please contact us to speak to a member of our team directly.