After economic shutdowns caused by the Covid-19 pandemic led to low levels of inflation in 2020, increased demand as countries opened back up created inflationary pressure in 2021, then Russia’s invasion of Ukraine in February 2022 led to significantly elevated inflation around the world.

Faced with rising living costs, employees often expect pay awards to match. However, ECA’s Salary Trends Survey shows that local staff will be disappointed in most regions, as despite higher than usual pay awards in both 2022 and 2023, they will be outweighed by the levels of inflation, leaving workers worse off.

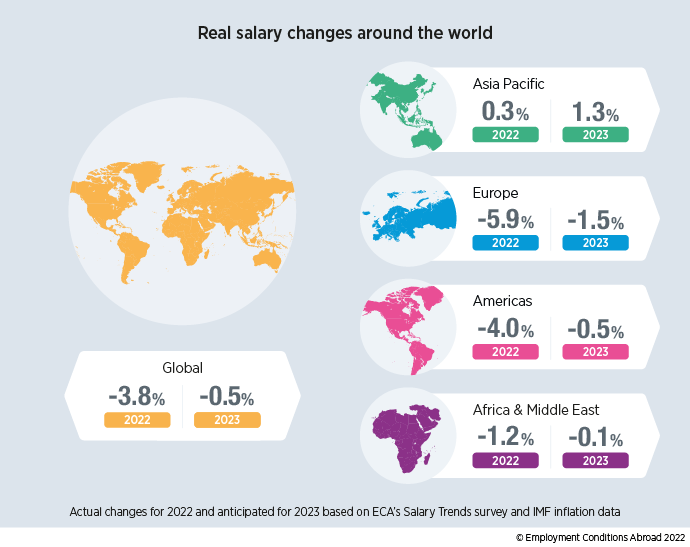

The real salary changes above are calculated by taking the average nominal salary percentage increase (i.e. the salary increase given to employees by their employers) and subtracting the inflation percentage. When they are negative, the buying power of the employee is lower than the previous year.

With inflation in 2022 being higher than forecast, nominal salary increases were also higher than companies had forecast in 2021 in the majority of countries. However, nominal salary increases rose by only 0.3% on average globally, whereas inflation was 5% higher than forecast. Employee buying power fell in more than three-quarters of countries surveyed in 2022, as employers failed to increase their pay awards to match higher inflation.

The outlook for 2023 is only a little more positive. Companies are expecting to offer higher wage increases and inflation is predicted to be lower than this year, but despite this, over half of countries are forecast to see real-terms decreases next year as well. Asia is the only region to buck the global trend and escape real decreases, with employees in the region seeing real increases in both 2022 and 2023.

Although there is an expectation that higher inflation leads to higher nominal salary increases, that is not always the case, as inflation is only one of the factors influencing pay awards. For developed countries in particular, average salary changes are consistent from year to year and reactions to changes tend to be delayed. In the USA, for example, average nominal salary changes (shown by the blue line below) have been slow to rise following the surge in inflation (shown by the red line) and only in 2023 will average increases rise above 4%, just as inflation is forecast to drop once more.

As this demonstrates, sudden increases in inflation do not always lead to employers re-evaluating their strategy straightaway. Companies frequently look to monitor the situation before making any changes, and it has often been the case previously that inflation cooled and returned to previous levels without any major changes to pay awards. In addition, the worsened economic climate can affect businesses, limiting employers’ ability to afford higher salary increases. For example, lower nominal salary awards provided around the world in 2020 were mainly due to the wider economic disruption caused by the Covid-19 pandemic rather than the fall in inflation specifically.

When there are sudden economic changes such as those we saw this year, the timing of annual salary reviews can also play a role. For those reviewing salaries in the first quarter of 2022, the subsequent spikes in inflation were unlikely to have been budgeted for. In many countries, the results show that companies reviewing salaries in the first three months of the year are forecasting higher increases for 2023 than those reviewing later in the year, as they are only now able to react to the economic changes for the first time.

With many countries now seeing double-digit inflation and the erosion of workers’ buying power, it is worth looking at these results in the context of locations where high inflation is more common. Results for these locations show that when inflation reaches extreme levels, it is rare to see employees receive pay increases to match, as such increases are unaffordable in difficult economic conditions.

In Argentina, although inflation and salary movements have been similar, local staff have seen salary decreases in real terms for many years as inflation has constantly outpaced salary growth. In 2023, even though Argentinian workers are forecast to receive the highest nominal salary increases in the world, inflation of 76% means they will feel a 26% salary decrease in real terms.

As we have seen with developments over the past year, forecasts can change significantly based on global events. However, unless inflation falls by more than expected, the pain is set to continue into next year for most.

FIND OUT MORE

The complex macroeconomic factors at play within the setting of salaries are covered in detail in ECA’s Salary Trends Reports which are published for over 70 countries and cities. The reports include graphical and tabular data plus economic analysis and, where possible, data for specific industry groups. Free to survey participants, they can also be purchased either individually or as a full set.

To find out more about the 2022 Salary Trends Survey and its findings, you can view the latest press releases on our News page.

The latest currency and inflation news is covered in ECA’s blog. You can sign up to follow our blog to receive notifications when new posts are published.

Please contact us to speak to a member of our team directly.